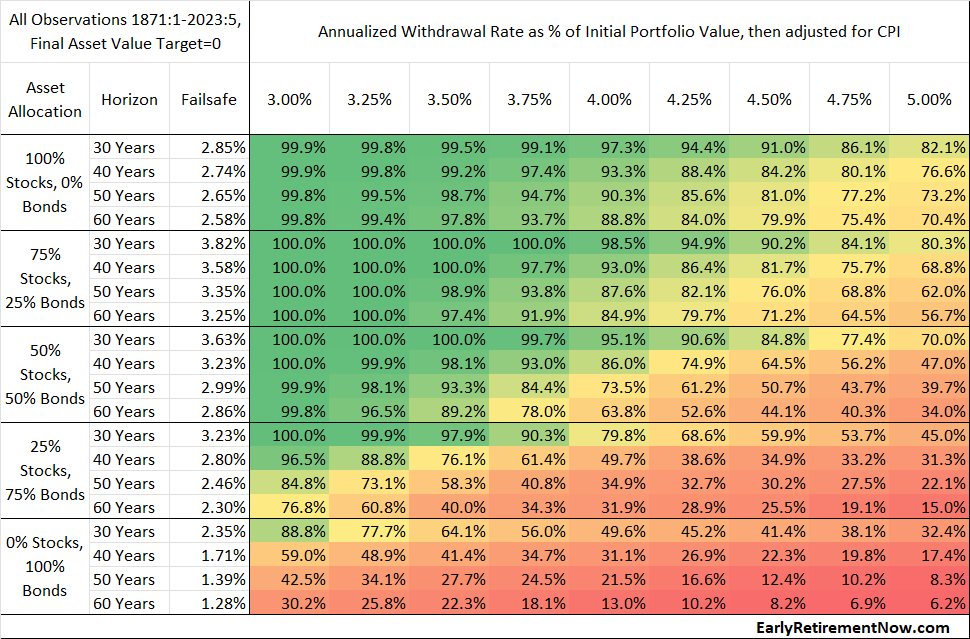

Understanding the 4% Rule Origins and Assumptions The 4% rule, introduced by financial planner Bill Bengen in the 1990s, revolutionized retirement planning. The rule was born out of a simple yet crucial question: How much can one safely withdraw from their retirement savings annually, without the risk of running out of money? The Trinity Study later validated Bengen's approach, confirming that a 4% initial withdrawal rate, adjusted annually for inflation, would likely allow retirees to maintain their nest egg for at least 30 years in most historical scenarios. Several key assumptions underpin the 4% rule: 30-Year Retirement Period : The rule was specifically designed for a retirement span of 30 years. Acceptance of Asset Depletion : The rule considers a scenario where, at the end of 30 years, your portfolio might be significantly depleted. As long as your funds last through your retirement, it's considered a success, even if there's little left for inheritance.…