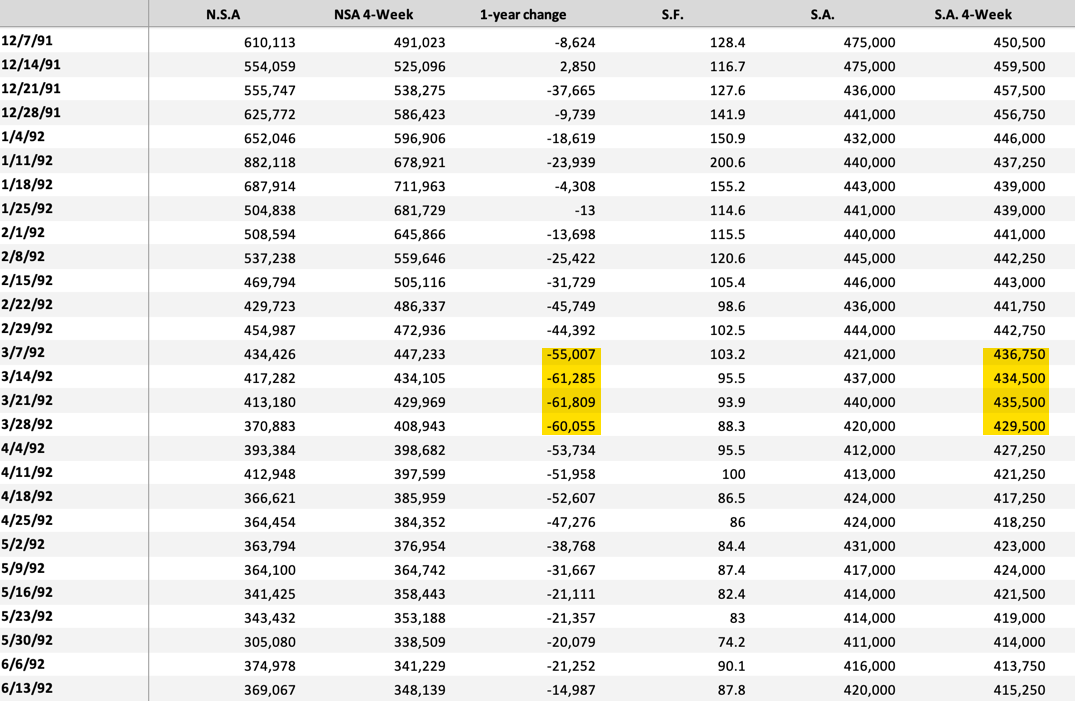

To understand the likelihood of the US Federal Reserve’s tapering timetable being accelerated, I believe we have to understand how quickly the US employment market improves relative to expectations. That’s because the Fed’s unstated bias in its dual mandate is toward employment over inflation given the talk of a K-shaped recovery and income and wealth inequality. So, let’s look at how jobless claims tracked at similar points in previous post 1982 jobs cycles. Why these comparables The reason I want to circumscribe the dataset to post-1982 recoveries is twofold. First, it’s because the post-1982 recoveries have all been ‘jobless’, i.e. slow to return to trend, starting with the 1990-91 recession. And secondly, they have all occurred in under the same rate-targeting fiat currency monetary regime. The Fed is likely to view these outcomes as baselines in their expectation for a return to normal.…